Today, many investors are concerned that inflation is coming back, and interest rates are on the rise. How would these factors impact private real estate investing? Many incorrectly think private real estate acts like how bonds do in rising interest rate environments (i.e. inflation rises, interest rates go up, bond values down). I don’t believe this is the case.

Why can private real estate handle higher interest rates?

First, you need to ask: “why are interest rates rising?” Most of the time, higher interest rates are driven by a stronger economy triggering inflation, leading to higher interest rates. Unlike bonds, which have a fixed coupon rate, private real estate has a variety of lease expirations for tenants. This allows sponsors to raise the lease rates as leases mature. A strong economy leads to the following enhancements to revenue:

- Higher rental rates – Rates can simply rise by inflationary pressures. However, the story is bigger. For example, In Albuquerque, New Mexico, where occupancy rates have hit the 96-97% range. Despite the COVID-19 impact, we were able to raise average rents on a particular multifamily property from $1,050/mo to $1,200/mo over the past year, a 14% rise. While this is an extreme example, it drives home the point that a strong economy leads to pricing power. As occupancy rates increase, rental rates can move much higher than inflation. Multi-family properties are especially positioned to handle inflationary pressures as lease terms are generally less than one year.

- Increased Occupancies – A stronger economy could also lead to higher occupancies (i.e. occupancy rises from 92% to 94%). This can be offset by new supply from new developments absorbing the increased demand from a stronger economy. So, in addition to increased revenues from higher monthly rental rates per unit or per square foot, we see higher gross revenues from higher occupancies.

- Lower Concessions – As the economy improves, tenants generally receive fewer concessions (i.e. one month free rent on a 12 month lease). One month free results in an 8% impact on revenue from one such lease. Concessions given to tenants vary based on the strength of the local market. Overall, we see concessions varying from about 1% to 3% per year of total gross revenue, depending on the strength of the economy and such local market.

- Lower Delinquencies – As the economy strengthens and unemployment drops, tenant’s ability to pay their rents due improves, which increases a property’s gross revenues as more tenants can pay their rent due.

What about higher borrowing costs from higher interest rates?

Certainly, higher interest rates will have an impact on the price that can be paid to acquire new assets. In the future, if rates rise, asset managers will be able to plan for the additional expense for new acquisitions.

For existing assets purchased before a significant move in interest rates, the impact to the property will depend on the debt structure chosen for such asset. Fixed-rate debt and floating-rate debt have very different scenarios.

For floating-rate debt, the costs will obviously increase as short-term rates increase. In general, a property will need to increase gross revenues by 5% to 6% for every 1% increase in interest rates to keep cash flows neutral (assuming about 60-65% leverage). So, a 2% increase in short-term interest rates will require a 10-12% increase in gross revenue to keep cash flow neutral. It is certainly possible that the four revenue enhancements above will more than offset this impact.

For fixed-rate debt, the higher interest rates from a stronger economy will greatly enhance cash flows as the fixed-debt is not impacted by any increases in short-term rates. So, all the revenue enhancements above will increase the cash flow to investors.

What about the impact of higher interest rates on a future sale? How high will cap rates go?

It is reasonable to expect cap rates to increase as interest rates go up. But, how much will cap rates be impacted by higher interest rates? Our bottom line: cap rates will be somewhat impacted by higher rates, but much less than the consensus.

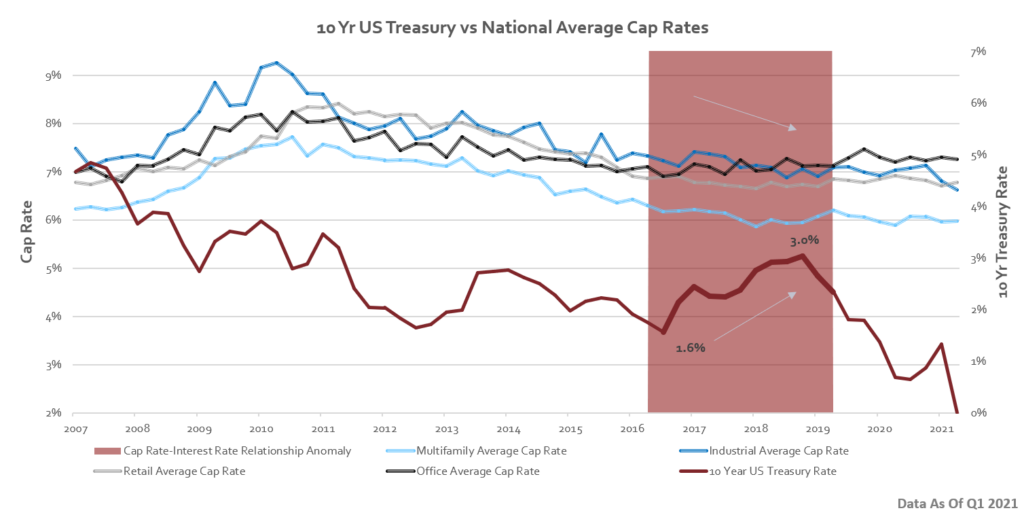

There are many factors that impact cap rates, interest rates being just one of them. In fact, history has shown that rising interest rates may not change cap rates. Reflecting on the 2016-2019 timeframe, the 10-year treasury rose from 1.6% to 3%, and average cap rates compressed, on average. Cap rates, actually, remained flat or decreased, despite the 10-Year U.S. Treasury Rate increasing by 1.5% during the same timeframe.

So, how could that have happened? There are other influences on valuation of private real estate. My view is that there are other factors, other than interest rates, that can impact real estate valuation:

- Availability of Debt – Real estate is heavily dependent on debt availability. Within the industry, most acquisitions use debt within the capital stack. It is a simple concept: More competition in the lending industry leads to a more competitive market and lower interest rates (caused by lower margins added to the index rate).

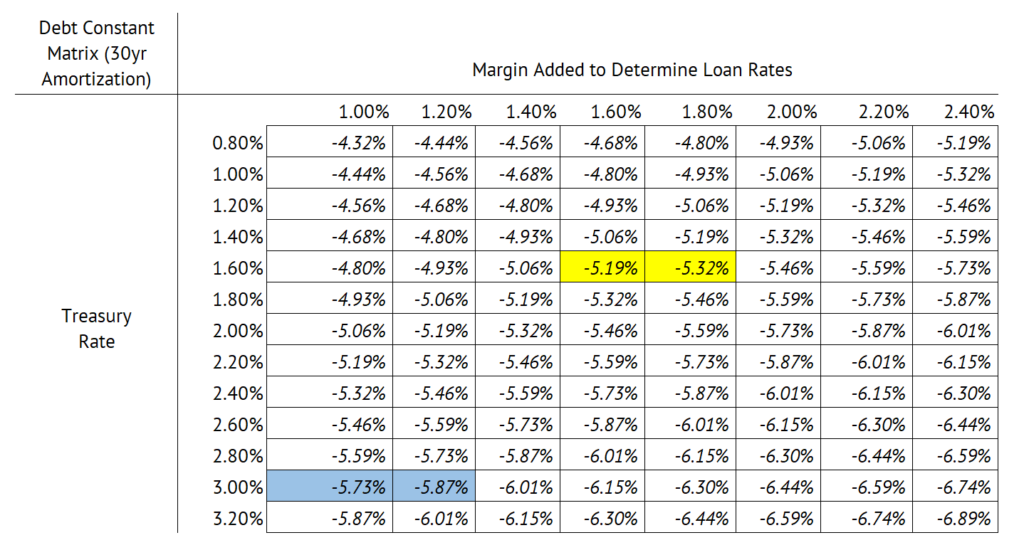

- Enhanced debt terms – The availability of creative debt terms enhances investor cash flows. For example, when lenders offer interest-only debt (i.e. no principal amortization), the debt constants (both principal and interest, combined) are much lower. For example, assuming a 3% 10-Year Treasury rate and a 1% margin, a borrower will be paying 4% annually on such debt with interest-only debt. Assuming a 1.6% 10-Year Treasury and a 1.6% margin, a borrower has a 3.2% interest rate and another 1.99% of principal amortization, for a total debt constant of 5.19% with amortizing debt. So, interest rates are important, but so are debt terms like interest-only.

- Availability of debt over various terms – Historically, as rates rise, the industry tends to fix rates for shorter terms like 5 or 7 years. Today, the 10-Year U.S. Treasury rate is 1.64%, the 7-Year is 1.29% and the 5-year is 0.87%. So, investors could reduce interest rate costs by fixing rates on shorter terms.

- Availability of Equity – Today, there’s an abundance of equity available for private real estate for a variety of reasons. Including: low correlation rate to public markets, high cash yields and its inflation hedge characteristics. Generally, more equity chasing the market leads to more aggressive valuations.

The Mathematics of Debt Constants and Cap Rates

Below is an example of the math behind an increase in interest rates and how it impacts cash flow.

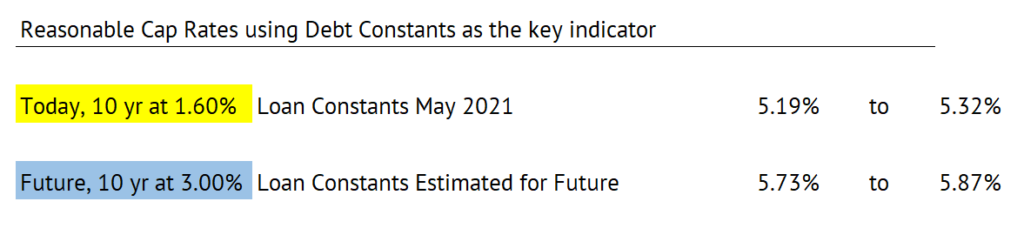

Our example above focuses on today’s market rate debt terms and compare to a potential 3.0% 10-Year Treasury rate. The margin added by a lender is along the X-axis. The Y-axis is the Treasury rate. Using simplified math, if the 10-Year treasury rate was 1.6% and if the margin rate adds about 1.6%, the total loan rates would equal about 3.2% with a 5.19% debt constant for amortizing debt.

In prior cycles, the margin added to the index dropped to a low of about 0.9 to 1.25%. With a 1.0% margin and a 10-year treasury rate of 3%, loan rates would be about about 4.0% or a 5.73% debt constant for amortizing debt. This is our best estimate of future loan rates with a 3% 10-year Treasury.

It’s our experience that cap rates do not move proportionally with interest rate changes. It is certainly correlated, but not proportionally. Cap rates are mostly impacted by debt constants (principal and interest), debt availability, and margin spreads.

As rates rise, margin spreads narrow, greatly reducing impact of higher rates. So, a move from 1.6% to 3% on the 10-year treasury, only changed the debt constant by 0.54% (5.73% vs 5.19%).

Therefore, you shouldn’t assume that a 1.4% move in interest rate will outright change cap rates by 1.4%. That 1.4% move in 10-year treasury likely only changes a debt constant by only 0.54%.

Today, cap rates for multifamily are trending from 3.75% to 5% depending on the quality of the asset, geography, market size or opportunity to create value. These cap rates are materially below the debt constants that assume full amortization of principal and interest. This results from the factors above like interest-only debt, and the abundance of debt and equity in the marketplace today.

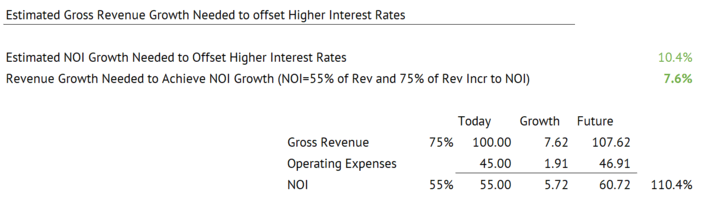

How much NOI growth is needed to offset the negative impact of a 3% 10 Year Treasury?

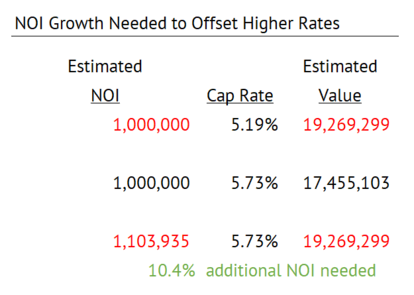

Overall, the math above estimates that we’d need gross revenues to increase by 7.6% to not have an asset’s value drop from interest rates raising by 1.4%. There are many assumptions in that example, but we think it’s a reasonably conservative estimate.

This assumes that the debt constants of fully amortizing debt have the most significant impact on cap rates. There are many other factors to consider like overall availability of debt and equity in the market.

So, here is the math of this estimate:

If the net operating income (NOI) of an asset was $1,000,000 at acquisition and cap rates move from 5.19% to 5.73% during the hold period, the NOI needs to grow by roughly 10.4% to offset higher cap rates to keep the value of the equity flat.

To achieve NOI growth of 10.4%, we are assuming that operating expenses are about 45% of the gross and that 75% of the Gross Revenue increase falls to the bottom line NOI. Gross revenue growth of about 7.6% from a stronger economy and enhanced revenues like higher rents, higher occupancies, lower concessions, and lower delinquencies results in no value loss from a move from 1.6% to 3% in the 10-Year Treasury. We believe that these are reasonable and believable assumptions and a pathway to no value loss from higher interest rates.

Is now a good time for Private Real Estate Investment?

There is much more to investing in private real estate than simply being a market timer. Real estate is a long-term asset class, is tax advantaged and a great diversification from the public markets of stocks and bonds. As an investor, diversification among asset classes is critical to wealth preservation. Real estate has unique characteristics – including low correlation rates to the S&P 500.

Interest rates are just one of many elements that impacts our investment decision in buying real estate investments. Human error in real estate will always allow opportunities to exist. Why do people sell off-market? Why do people not raise rents to market levels? Why not improve your assets? We don’t know why these things happen, but we certainly are appreciative of these opportunities in private real estate. Don’t let the possibility of higher interest rates scare you away.

In fact, real estate today is uniquely positioned as a great inflation hedge and interest rates will likely only have a minor impact on investment performance.

MLG Capital bases its real estate investing strategy on the dynamics of the market at the time of purchase, viewed through a local and national lens. Our strategy is then combined with a critical concentration of targeting NOI growth by identifying human error in property operations or market conditions that are favorable going forward. This strategy allows us to find opportunities no matter what part of the market cycle we happen to be experiencing.

Combining this tailored strategy with a proactive approach to improve cash flow and valuation – not relying on the market to just “buy low, sell high” – we’re able to execute our mission: delivering consistent and impactful value to our investors.

Want to speak to an expert? Start your journey with MLG Capital today.

Timothy J. Wallen, CPA, is a Principal and the Chief Executive Officer of MLG Capital. He’s passionate about family, traveling, golf and skiing. Outside of work, you’ll likely find Tim spending time with his family, or traveling.