We’re all familiar with the sentiment surrounding “there’s risk present in every investment”, and this holds true for private real estate. As investors consider the plethora of allocation options available to them in today’s connected world, it’s important to be aware of the potential risks present in any investment.

All too often, people will dive into a deal because it touts a high Internal Rate of Return (IRR) on paper, but they fail to take any time to peel back the onion and analyze the set of assumptions that lead to that shiny number. While there are certainly several variables that impact the risk/reward of an investment, one of the most overlooked items is how much debt, otherwise known as leverage, a manager is using to finance the deal.

Let’s take a deeper look at how increased leverage can enhance the returns generated by an investment, while it also inherently increases the risk to the investor.

Why Leverage?

For anyone who is a homeowner, you likely already understand the implications of debt financing without even realizing it. The concept is simple – if you put 5% down on your home and borrow 95% from the bank, your monthly payment will be larger than if you put 40% down and only borrow 60% from the bank. This same concept holds true in private real estate investing. Though, in a different context, using leverage can maximize returns for investors. But, what risks are you taking with higher leverage?

Typically, higher leveraged deals will promote a higher overall targeted return due to the risk factor. Higher targeted returns should always be taken with a grain of salt, especially when looking at the risks vs. the reward.

My advice? Do your due diligence on how the manager feels about debt and dig into their targeted and realized returns vs. their historic and current leverage points.

For example, a value-add multifamily deal may be less attractive (in terms of risk) if it is levered at 80% loan-to-cost (LTC) to hit an overall annualized return of 15%. A higher LTC can dramatically increase the risk of loss for invested equity.

On the other hand, a value-add multifamily deal targeting a 14.5% overall rate of return, at 65% LTC targets lower risk of loss for invested equity while hitting similar returns.

Comparing Scenarios

Suppose an asset is for sale for $10,000,000, has an expense ratio of 50% each year and produces $500,000 of net operating income (NOI), which is a 5% cap rate. The three scenarios below look at how capitalizing this deal in different ways can impact the cash flow and inherent risks to the investor.

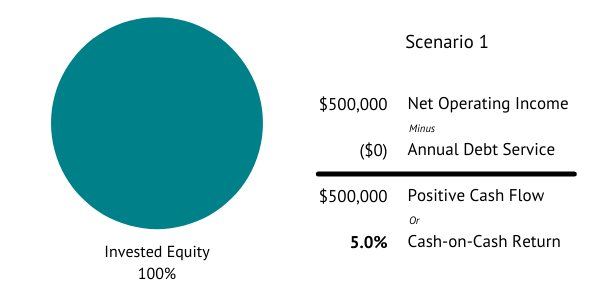

- 0% Leverage – All cash acquisition

If an investor were to purchase this asset with $10 million cash, they would be responsible for no mortgage payment and would realize a 5% cash-on-cash (CoC) return on their $10 million. This rate of return is equal to the acquisition cap rate of 5%, otherwise known as the unlevered yield produced by the investment.

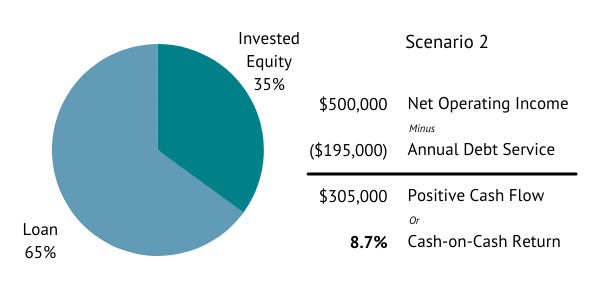

- 65% Leverage

Suppose a different investor who seeks to buy this asset decides to take out a loan for $6.5 million, or 65% of the purchase price. For easy math, assume this is an interest only, 30-year amortization, loan at a 3% interest rate, resulting in an annual debt payment of $195,000. In this scenario, instead of having to come up with $10 million, the investor only has to bring $3.5 million to the table, but the purchased asset is still producing the same $500,000 of NOI. This investor is generating positive cash flow of $305,000, equal to an 8.7% CoC return on their $3.5 million investment.

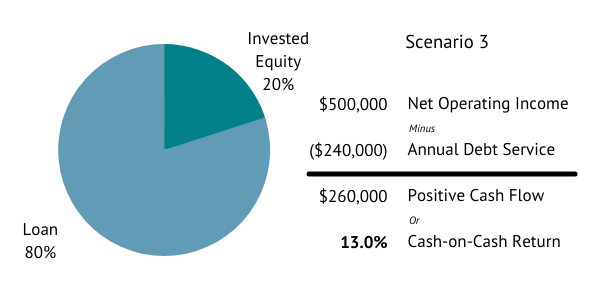

- 80% Leverage

Suppose a third investor comes along who has a real appetite for risk and decides to buy the asset by taking out an $8 million loan, or 80% of the purchase price. Like scenario two, this investor takes out an interest only, 30-year amortization, loan at a 3% interest rate, resulting in an annual debt payment of $240,000. For this investor to acquire a $10 million asset, they only need $2 million of cash. Regardless of the financing, the underlying asset still produces the same $500,000 of NOI, which results in positive cash flow of $260,000, equal to a 13.0% CoC return on their $2 million investment.

These scenarios demonstrate that using higher leverage can enhance the projected returns on an acquisition.

What’s the catch? Why would you not want to use maximum leverage to maximize your potential returns?

Risk, or understanding DSCR

Lenders assess risk by focusing on how likely the NOI from an asset is to cover required debt payments. This is called the Debt Service Coverage Ratio (DSCR). Generally, the higher the DSCR the lower the risk of the investment.

Let’s revisit the two examples from above that utilize some leverage and look at their debt service coverage ratio.

As a refresher, we are assuming the purchase of a $10 million asset, which generates a $500,000 annual NOI. We are also assuming a 3% interest-only, 30-year amortization loan in each scenario, regardless of interest only or principal and interest payments, at the leverage percentages below.

65% Leverage: $500,000 (NOI) / $195,000 (Annual Debt Service) = 2.564 (DSCR)

80% Leverage: $500,000 (NOI) / $240,000 (Annual Debt Service) = 2.083 (DSCR)

A DSCR above 1.25 will garner the attention of most institutional lending options. Under these assumptions, both leverage points appear to adequately service their debts.

However, what happens at the end of an interest-only period when principal payments need to be made? Let’s return to scenarios 2 and 3.

Scenario 2:

65% Leverage: $500,000 (NOI) / $328,848 (Annual Debt Service) = 1.520 DSCR

In this example, you would be able to sustain a reduction of ±34% in NOI, and still be able to service the debt payment. This would also be referred to as the “break-even point.”

$330,000 (Adjusted NOI) / $328,848 (Annual Debt Service) = ±1.00 DSCR

Scenario 3:

80% Leverage: $500,000 (NOI) / $404,736 (Annual Debt Service) = 1.235 DSCR

In this example, the break-even point would only allow for a reduction of only ±19% in NOI. In addition, the DSCR on the fully amortized payments dropped below the minimum standard for most institutional lenders, being the 1.25 threshold. This would result in the need to seek alternative lending options upfront, often with less favorable terms and policies.

$405,000 (Adjusted NOI) / $404,736 (Annual Debt Service) = ±1.00 DSCR

Key Takeaway: Not too low, not too high. Less than maximum leverage is ideal.

In our Private Funds, we target debt leverage at 60-65% of all-in costs on a consolidated basis, which is lower than many real estate sponsors in our industry. Because we target lower leverage, we can handle a larger drop in NOI.

Using leverage at a reasonable level has allowed our investments to produce risk-adjusted returns for investors and an average 2.20x equity multiple1,3 on invested capital, for all sold deals. For every dollar invested, $2.20 dollars were returned to investors, since our inception in 1987.

Want to learn more? Happy to connect on LinkedIn. If you enjoyed this read, then you may also enjoy one of my other articles about different industry investment return structures. Check it out.

Jorjio Hopkins is a Senior Associate at MLG Capital, with a master’s in real estate and passion for service. He served for a number of years as a Marine Corps officer and as a dance lead for his high school show choir. Connect with Jorjio on LinkedIn. Or, if you’re an accredited investor, consider investing with us.