The end of January each year brings with it the unofficial kick-off to the new year in the world of the multifamily industry at the National Multifamily Housing Council’s Annual Conference. The conference brings together 8,000+ multifamily industry professionals including owners, equity investors, debt providers, property managers, you name it – they are in attendance (Source: NMHC.org). The conference brings with it a look back on the prior year, but more importantly, a forward look to the next year of what the industry expects to see. Think thousands of executives, investors, lenders, and strategists from across the country, all converging for a week of market intelligence, networking, and candid debate about the future of rental housing. It’s where the pulse of multifamily is taken, trends are dissected, and real-time sentiment filters through the noise. And of course, it offers MLG an opportunity to connect with peers to further enhance our relationships with brokers, lenders, and other owners to continue to strengthen relationships and source the best investment opportunities for our investors.

If I had to summarize the main takeaway and theme for 2026 based on numerous conversations MLG teammates had at NMHC, it would be the following: equity flows, where rent grows. To investors that may not seem like a novel concept or strategy, but where that takeaway really stems from is the continued operational challenges that short term excess supply can cause on certain markets and submarkets across the country. Our belief is that supply and demand drive operational performance locally, submarket by submarket. While this fundamental principle of economics should be straightforward in concept, this principle is most often challenged or put out of balance in the world of real estate with excess supply.

Supply (and Demand)

- Supply and demand make up the equation; however, as outlined below, the industry challenge today is mostly on the supply side of the equation. Location, location, location goes the real estate adage. This is still true, many today would likely argue supply, supply, supply is the main focus.

- Demand has a few challenges with slower population growth in 2025 (i.e. reduced immigration) and associated household formation growth, but lack of single-family housing, delayed marriages, desire to rent longer results in continued absorption & sustained demand (Source: U.S. Census Bureau, 2024).

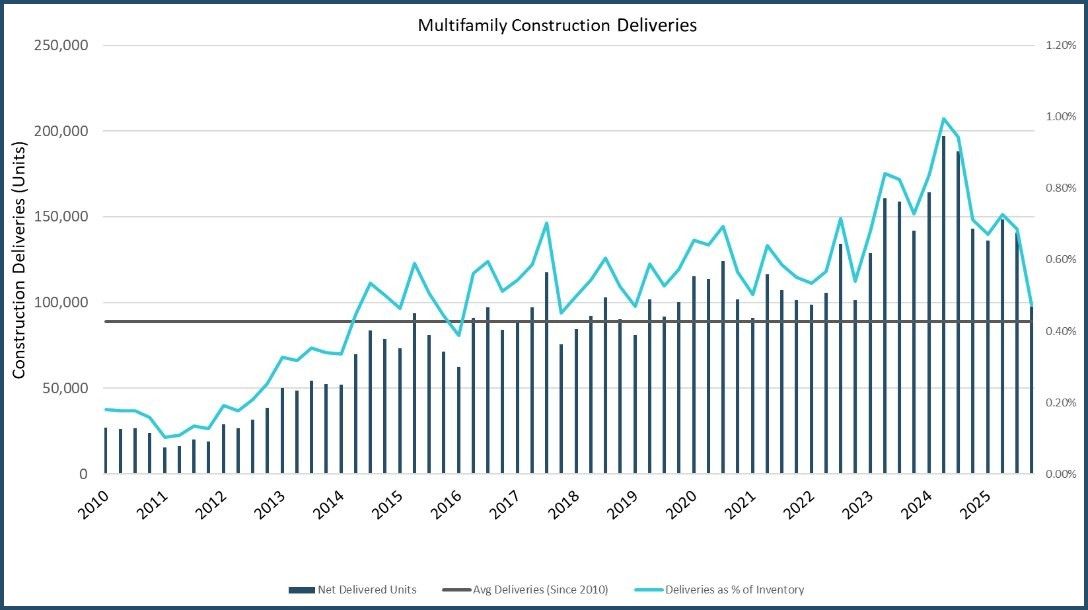

- Deliveries nationally are decelerating from ~600k+ in 2024 (the highest in five decades) to ~400k in 2025, with ~300k expected in 2026 and the mid‑200k range is projected for 2027 (Source: CoStar, Q4 2025).

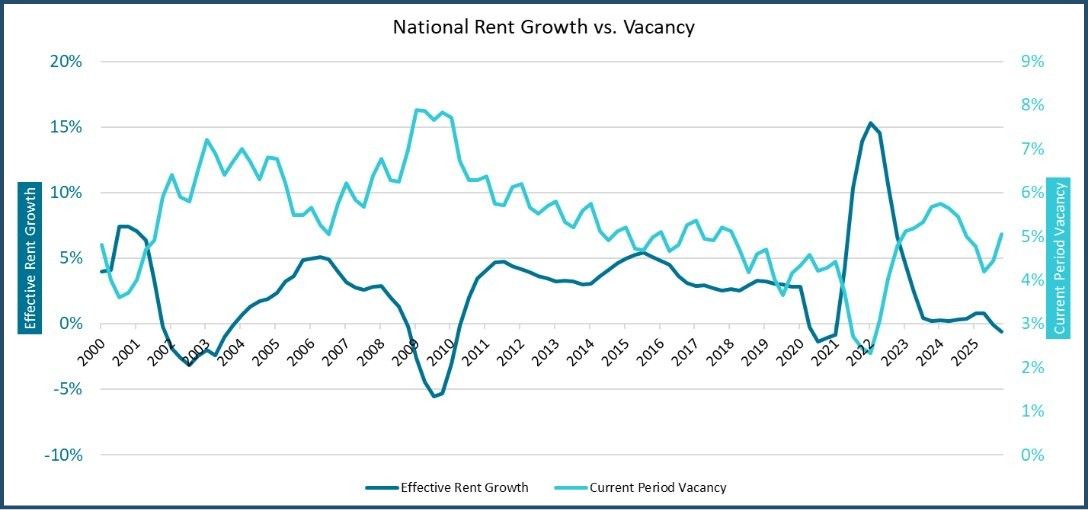

- Absorption remains real but increasingly expensive in supply‑dense markets; in 2025, renewal rents averaged +3.8% compared to ~–2.5% for new‑lease trade‑outs, highlighting renewals as the primary driver of revenue performance (Source: RealPage, Q4 2025).

- Industry rent growth expectations sit around ~2% for 2026, gradually trending back toward long‑term norms of ~3% in subsequent years (Source: RealPage, Q4 2025).

- But where is this supply? Not all supply is created equal. Most new supply is concentrated in high‑growth Sunbelt and Mountain West markets, where developers followed strong population and job expansion (Source: RealPage). In contrast, MLG is prioritizing markets with that we believe have a healthier balance of supply and demand.

- Fund VII’s initial investments have targeted assets that we believe have demonstrated steady, more predictable operational performance and cash flow in markets with more balanced supply and demand. Early allocations have focused on the Midwest, Pacific Northwest, and Mid‑Atlantic, regions where new supply remains comparatively limited.

Source: CoStar (Q4 2025)

Source: RealPage (Q4 2025)

Transaction Volume Expectations

- 2025 saw an increase year over year. There was a positive sales volume trend in 2025 with total multifamily sales volume up 9% to $161B (per CBRE). Based on our conversations, most industry professionals expect more volume in 2026 for the following reasons:

- Bid/ask spread has narrowed and pricing/consensus has settled in.

- The renewed consensus is bringing buyers and sellers back into alignment, and many sellers are now more willing to transact after sitting out the past few years due to uncertainty.

- We expect to see more distressed opportunities brought to market—primarily driven by lenders or equity partners. These distressed sales generally fall into two categories:

- Newer construction in high‑supply markets that have struggled to stabilize or are leasing at rents below original projections due to heavy competition.

- Workforce housing (Class C) properties facing operational strain, including higher delinquency, limited ability for residents to absorb rent increases, and rising repair/turnover costs. Investor demand has shifted accordingly, and we have observed returns on Class C workforce housing are now at their widest spread relative to Class A and B assets since the Global Financial Crisis.

Equity

- The general sentiment is that investors will continue to target multifamily and industrial as the most favored asset classes. Significant equity desires to invest in the long-term fundamentals multifamily investments provide.

- This equity will be selective and focused on markets with strong fundamentals and predictable cash flow. MLG has been investing with this mindset and focus and will continue to do so across our direct and joint ventures strategies.

Debt

There is likely no shortage of debt availability in 2026. The banks are back, adding to higher agency allocations in 2026 ($88B each for Fannie & Freddie; up 20% YOY) and active lenders across life companies and private credit including debt funds, preferred equity and mezzanine debt (Source: US Federal Housing Finance Agency). We believe that the large amount of private credit raised but not invested over the last 2-3 years is hungry to be invested and returns have compressed.

Investors continue to focus on positive leverage at closing or in the first year after closing.

MLG Focus & Strategy

Our focus is unchanged and, I’d argue, appropriately boring: generally targeting new investment opportunities in well‑located A & B assets in submarkets with supply/demand balance with lower forward supply. Over the last three years, wage growth in this cohort has outpaced rent growth at the national level, supporting collections and reducing delinquency risk compared to more economically vulnerable segments (Source: RealPage and Federal Reserve Economic Database, 2024). That’s where we see the most durable cash flow today.

Upside Potential

As we primarily focus on investments in areas of supply and demand balance, we continue to review opportunities in high supply areas as well. These investments receive a heightened focus and scrutiny but may present the opportunity to acquire an asset being sold precisely at the wrong time. Acquiring quality assets in higher supply submarkets at significant discounts to replacement cost could provide outsized return potential as markets stabilize, concessions burn off, occupancies rise, and rent growth is achieved.

We believe that as operational performance returns across submarkets, investor capital is expected to return and likely help drive stabilized returns back to typical levels.

Disclaimer

Securities offered through North Capital Private Securities, Member FINRA/SIPC. Its Form CRS may be found here and its BrokerCheck profile may be found here. NCPS does not make investment recommendations and no communication, through this website or in any other medium, should be construed as a recommendation for any security offered on or off this investment platform.

This article is intended solely for accredited investors. Investments in private offerings are speculative, illiquid, and may result in a complete loss of capital. Past performance is not indicative of future results. Prospective investors should conduct their own due diligence and are encouraged to consult with a financial advisor, attorney, accountant, and any other professional that can help them to understand and assess the risks associated with any investment opportunity.

This offering includes risks and uncertainty many of which are not outlined herein including, without limitation, risks involved in the real estate industry such as market, operational, interest rate, occupancy, inflationary, natural disasters, capitalization rate, regulatory, tax and other risks which may or may not be able to be identified at this time and may result in actual results differing from expected.

Advisory services offered through MLG Fund Manager LLC, an investment adviser registered with U.S. Securities & Exchange Commission.